As consumer debt climbs, so does demand for professional services that help creditors recoup those debts. The debt collection industry is projected to grow at a compound annual growth rate of 4.0% from 2022 to 2028. With more lending and borrowing happening every day, debt collection services will only become more essential over the next decade.

This comprehensive guide breaks down how to start a debt collection agency from the ground up. From obtaining licensing to leveraging technology to improve recovery rates. With the right skills and systems in place, you can carve out your niche in this rapidly expanding industry.

1. Conduct Debt Collection Agency Market Research

Market research is important when starting a debt collection business. It provides details into your target market, competing debt collection companies, the debt collection process, and trends in debt collection business services. As a debt collection business owner, market research is invaluable.

Some information you’ll learn through market research to form a successful debt collection agency includes:

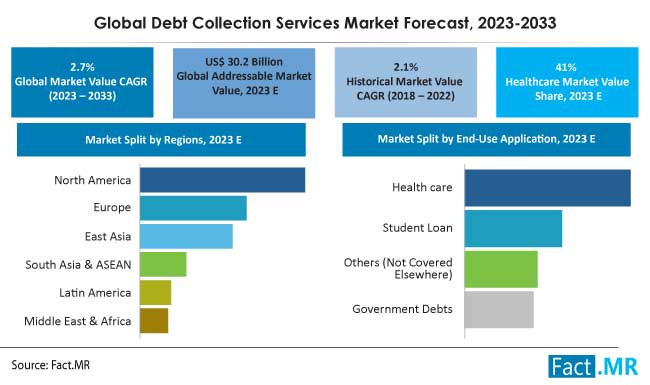

- Private creditors, including credit card companies, hospitals, utilities, and telecoms cumulatively extend over $870 billion in consumer credit annually.

- With U.S. household debt recently hitting a record $16 trillion, the need for collection services continues rising in tandem.

- Geographic location also plays a role in shaping profit potential.

- Launching operations near major metro areas increases visibility among high volumes of prospective creditor clients.

- Existing competition creates another critical analytical element.

- After thoroughly analyzing the current debt collection landscape, the opportunity appears rife to establish a lean, niche-focused agency.

- Between soaring consumer debt, creditor demand, positive growth metrics, and low barriers to entry, the market contains abundant potential.

- Strategic positioning combined with tenacious recovery practices could certainly yield a prospering new enterprise.

All the details learned through market research, including information on obtaining your debt collection license and local debt collection laws lead to a solid business plan.

2. Analyze the Competition

Doing your homework on competitors represents a vital step when launching any new business, including a debt collection agency. A few key areas to analyze surrounding rivals in your geographic territory include specialization, technologies leveraged, and online presence and reviews.

Many agencies concentrate efforts on specific industries or debt types. For example, some focus exclusively on bank credit card debt while others pursue overdue medical payments or government-backed student loans. Identifying gaps where competitors may currently be overlooking provides an opportunity to establish a niche.

Evaluating technologies competitors have integrated can also reveal areas for differentiation. Cloud-based practice management tools, predictive dialers, mobile apps, data analytics, automatic payment processing, and customizable CRM now help modernize collection operations.

Checking online profiles and reviews enables assessing the reputation of established nearby agencies as well. Resources to consult range from basic Google searches to detailed reports from the Better Business Bureau highlighting complaint volumes over time.

While the debt collection space stays fragmented regionally, understanding the competitive landscape in a local market enables identifying advantage areas to exploit. Carving out a niche and embracing the latest technologies under a model committed to integrity from day one establishes differentiation that converts to client wins.

3. Costs to Start a Debt Collection Agency Business

Getting a new debt collection agency off the ground requires upfront investment like any small business. From registering your legal entity to leasing office space and purchasing equipment, essential start-up costs arise.

Startup Costs

- Beginning with legal and regulatory fees, expect around $800 to formally register your business.

- Average small office suite rentals range from $1,200 to $1,800 monthly.

- Second-hand desks and chairs provide cost-effective options, usually between $50 to $150 per workstation.

- Investing in a cloud-based phone system removes the need for a costly on-site setup, and most offer call routing and tracking essential for collection work. Top providers offer packages of around $20 per user monthly.

- Hiring staff is costly. Experienced negotiators earn around $30,000 to $40,000 annually, with top performers potentially making up to $60,000 including commission incentives.

- Dedicated office assistants land between $15 and $18 hourly. Attempt to keep payroll below 30% of total revenues.

- Altogether, launching a compliant 4-person collection shop with bare business essentials requires roughly $15,000 to $20,000 in start-up capital.

Ongoing Costs

- Allocating marketing spend for continuing lead generation and referrals equates to between 5% and 10% of quarterly collections—or a minimum of around $2,000 every month.

- Technology also commands continuous investment. From database access fees to keeping hardware and software current, stay ready to dedicate another 5% to 10% of collections toward your stack.

By upholding robust infrastructure, skilled staff, and ethical processes, a lean agency minimizes risk while clearing profitability within the first year of full operations. Carefully budgeting for essential start-up and ongoing costs from the outset paves the way for lasting returns.

4. Form a Legal Business Entity

When establishing a debt collection agency, the legal structure you select dramatically impacts everything from day-to-day operations to tax burdens and personal liability. While sole proprietorships offer the easiest route with minimal upfront costs, limited liability companies (LLCs) best shield your assets from risk exposure.

Sole Proprietorship

Launching as a sole proprietorship means the business stays wholly tied to you as an individual. You’re entitled to every profit, but also shoulder unlimited personal responsibility for debts and legal actions against the company. Any court judgments stemming from perceived FDCPA violations or complaints directly target your possessions.

Partnership

Formal partnerships enable combining resources and expertise with one or more co-owners. However, each partner remains equally liable for collective business liabilities. Disagreements between partners may also impede quick decisions during daily operations.

Corporation

Establishing the agency as a standard corporation creates the highest level of red tape. Corporations face extensive record-keeping surrounding shares, director meetings, votes, and more. You also take on added tax complexities like double taxation on profits. For small debt collection teams, this steep learning curve’s benefits rarely outweigh the extra costs.

Limited Liability Company (LLC)

Registering your agency as an LLC from day one restricts exposure of personal assets to lawsuits and judgments solely tied to company actions. Only your investment and holdings in the business itself enter jeopardy. The flexible structure accommodates easily adding new members or foreign investors moving forward.

5. Register Your Business For Taxes

Before legally operating any business, registering for the proper tax IDs ranks as an essential step. At the federal level, sole proprietors can use their Social Security Number instead. However, all other structures including LLCs must obtain an Employer Identification Number (EIN).

The IRS issues EINs exclusively for tax reporting purposes. An EIN essentially functions as an SSN for your business when opening business bank accounts, applying for financing, hiring employees, and filing tax returns.

Securing an EIN proves quick and convenient through the official online IRS application. You can expect to receive your EIN immediately after submitting confirmations for details like business name, address, and entity structure details.

Navigating to Irs.gov and selecting the “Apply Online Now” link begins the streamlined process. Ensure that you have your taxpayer ID handy as well as knowing your start date.

The IRS charges no fees to obtain an EIN, whether applying online or mailing paper forms. You’ll also use your fresh EIN for registering within your home state’s taxation department for sales and use tax obligations. These permits allow legally collecting and remitting owed state taxes later on.

Depending on your state, expect to pay less than $100 for standard seller’s permits and tax certificates. For example, Texas charges just $17 for their state sales tax permit. However, amounts vary widely across the country. Ensure checking with your state revenue division for precise local registration costs.

6. Setup Your Accounting

Maintaining meticulous financial records remains non-negotiable when launching a debt collection agency. Unlike product sales or service invoices, your accounts receivable income derives from highly regulated debtor agreements. One minor accounting misstep could quickly snowball into FDCPA violations, lawsuits, and business-crippling penalties.

Accounting Software

Getting set up on small business accounting software like QuickBooks from the start streamlines everything from sending invoices to tracking payments. QuickBook’s collection-specific template enables the seamless generation of itemized statements detailing interest, fees, and principal balances owed.

Hire an Accountant

While certainly feasible for sole owners to self-manage daily bookkeeping tasks using platforms like Quickbooks, consider retaining an accountant at least for yearly filings and tax prep. Expect rates between $800 and $2,000 for individual returns, and $1,000 to $5,000 for partnerships and LLCs.

Open a Business Bank Account

Just as critical, set up a dedicated business checking account immediately to bifurcate personal and agency funds. Never commingle expenses across sources or tap company coffers to cover a personal cost shortfall. Doing so muddies the financial water and intensifies headaches for your accountant and at tax time.

Apply for a Business Credit Card

As your venture scales, applying for a small business credit card also simplifies tracking. Business cards get approved and assigned limits based primarily on your credit score for newer agencies. Get cards with up to $100,000 in potential financing and cash back or travel perks tailored specifically to maximizing value for small professional services firms.

7. Obtain Licenses and Permits

Before operating a debt collection agency, securing proper credentials from state and federal regulatory bodies remains obligatory. Find federal license information through the U.S. Small Business Administration. The SBA also offers a local search tool for state and city requirements.

At a minimum, registering with the attorney general’s office within your home state stands necessary. Expect costs between $50 and $500 depending on specific location rules. This process often coincides with formally creating your business identity as an LLC or corporation depending on the selected structure.

Check your intended county and city to determine if additional local business permits apply as well. For example, Philadelphia requires all professional services firms to obtain a commercial activity license with fees based on number of employees. Pittsburgh levies a roughly $100 business privilege tax. Ensure researching regional and municipal permit requirements based on the headquarters address.

Confirming licensure with the Consumer Financial Protection Bureau also makes the list for those focused strictly on first-party consumer debt accounts. Registration takes place on the CFPB Debt Collector portal and renews every year for $100, regardless of agency size. These clearances help reassure customers of adherence to fair practices.

However third-party agencies contracting as outside servicers for the Department of Education federal student loans instead answer to the Department’s Direct Loan Program. Annual renewal here runs $750 and carefully examines elements like years in business, complaint ratios, litigation history, and financial stability through corporate tax returns.

Card issuers like American Express, MasterCard, and Visa could mandate their additional credentialing as well before officiating a servicing contract. Larger banks and creditors likely follow suit with formal vetting procedures surrounding definition rates, security, accessibility policies, and collector expertise areas.

8. Get Business Insurance

Insuring your fledgling debt collection agency safeguards from scenarios that could otherwise devastate your operations. Policies cover specific exposures like property damage, employee injuries, and professional liability that stand primed to arise within daily collection workflows.

For example, not carrying adequate property protection means personally funding full office repairs or replacement if a fire, flood, or theft incident strikes. Just a single destroyed server or software platform could halt calls and cause missed client targets.

Another unchecked risk – collection representatives working onsite without injury coverage opens you to cover their lost wages or disability care costs entirely out-of-pocket after a workplace fall or contracting COVID-19, which could run tens of thousands without sufficient insurance.

Insuring against professional liability keeps your assets shielded if a creditor sues over perceived FDCPA violations or consumers launch complaints surrounding your agency’s practices. While cases may stay baseless, legal defense fees alone easily exceed $30,000 should regulatory run-ins occur.

Gaining quotes from leading small business insurers like CoverWallet starts by specifying your entity structure, office location, and number of employees. Expect total yearly premiums for essential protection spanning property, general liability, and professional coverage to run from $1,200 per year for single LLCs upwards to $5,000 annually for 10-person teams.

Use Next Insurance’s handy instant quote builder here to calculate your initial target number based on the scope of operations. Their streamlined claims processes also simplify handling troubles when issues ultimately emerge.

9. Create an Office Space

While technological automation enables remote workforces, establishing a physical office presence often bestows heightened credibility for financial services providers like debt collection agencies. When meeting with prospective enterprise creditors and banking partners on-site, on-demand access to professional work areas stays key.

Home Office

For solo owners operating from home, dedicating space to an ergonomic workstation and data-secure computer hardware removes household distractions during customer-facing interactions. Expect costs ranging from $100 to $300 for the basic table, chair, and machine investments. However, collaborating with partners or employees would soon require an upgrade.

Coworking Office

Seeking out a coworking space membership enables on-demand meeting rooms, call booths, event hosting, and front-desk staff assistance as your agency scales from a one-person shop to a fully-fledged workplace. National operators like WeWork provide flexible month-to-month access to workspace pods, private offices, wi-fi, printers, conference spaces, and more for roughly $300 to $800 monthly.

Commercial Office

Eventually securing traditional office suite leases within commercial buildings proves necessary for larger collection teams and enterprise partners preferring an established professional presence. Expect rents between $20 and $35 per square foot in most metro regions for spaces accommodating 10 or more staffers.

10. Source Your Equipment

Launching a debt collection venture hinges on the technology empowering a remote workforce to drive recoveries. While software represents the brains, call center hardware forms the backbone enabling seamless communication with credit issuers and delinquent account holders.

Buy New

Brand-new computers, headsets, phones, and printers certainly equip teams with the highest-performing gear backed by warranties. Shopping mainstay retailers like Amazon and Best Buy offer all categories affordably. For example, desktop phones with HD voice clarity start around $75. Brand new HP LaserJet printers cost approximately $300.

Buy Used

Sourcing quality refurbished or lightly used equipment stands as an economical alternative. eBay and Craigslist listings consistently showcase enterprise-level Cisco phone systems, 15-inch HP/Dell LCD monitors, and high-capacity printers often discarded from office upgrades available under $250 in total. Facebook Marketplace also boasts reputable nearby dealers.

Rent

Renting subscription plans for hardware needs also balances flexibility with budgets. National chains like Rentacomputer pioneer month-to-month rentals on workstations, servers, network infrastructure plus video conference equipment with nationwide drop shipping. Costs scale from $60 laptop and phone bundles to $500 high-volume copier/printer combos supported by replacement guarantees.

Lease

Leasing over longer 12 to 36-month terms works best aligning with initial office space contracts for larger teams. Options like Dell Financial Services cover technology lifecycle management, they ship pre-configured devices like wireless headphones and desktop computers then facilitate upgrades or migrations as needs evolve. This helps limit heavy one-time investments carrying overlap risk.

11. Establish Your Brand Assets

Cultivating a professional brand presence fuels recognition, trust, and ultimately new client acquisitions for debt collectors. Investing in assets reflecting integrity and competence at launch builds equity other agencies can’t easily replicate later.

Get a Business Phone Number

Centralizing communications under a dedicated business phone number adds legitimacy to inbound calls and client meetings. Services like RingCentral offer custom toll-free and local numbers routed to any device for as low as $30 monthly. Call management features like greetings, IVR menus, voicemail, and call forwarding project enterprise-grade infrastructure.

Design a Logo

Creating a sleek, memorable logo also makes an impression. Looka’s AI-powered logo maker helps craft icons, color palettes, and typefaces aligned to your vision within minutes starting at $20. Opt for simple, authoritative marks, think scales, columns, or snippets of legal scrolls – that iconize fairness and establishment.

Print Business Cards

With a visual identity set, order business cards, letterhead, and office signage from Vistaprint. Their economy card stock still exudes professionalism with prices ranging between $10 and $50 depending on volume, design complexity, and paper grades. Expect building signage and indoor directionals to run $50 each.

Get a Domain Name

Staking a domain builds SEO visibility and directs client inquiries to conversion journeys. Services like Namecheap facilitate registering.COM domains for under $10 the first year and then $15 thereafter annually. Align to your business name or locality for memorability.

Design a Website

Building out a lead-generating website fuels credibility among prospective creditors evaluating your capabilities. Solutions like Wix make launch easy with adjustable templates, analytics, and secure payment integration for as low as $14 monthly. For those preferring custom site coding, Fiverr freelancers provide professional site mapping and programming services starting around $500.

12. Join Associations and Groups

Plugging into associations and peer groups fuels growth for new debt collection agencies by enabling the exchange of insider knowledge and direct referral opportunities.

Local Associations

Joining your state collection association connects you with regional peers targeting the same creditor relationships. Membership fees hover around $300 annually but grant database access to top area talent along with newsletters detailing recent case law precedents that could impact practices. Try the Association of Credit and Collection Professionals to start.

Local Meetups

Attending local industry meetups also pays dividends for putting faces to names of potential big fish partners like bank attorneys, credit executives, and fellow subcontracted agencies. Sites like Meetup simplify finding these engagements, whether niche roundtables or large trade conferences. Expect investing two days quarterly to nurture lead sharing, troubleshoot issues, and benchmark performance.

Facebook Groups

Informal online communities stand primed to deliver advice as operations scale too. For instance, the Professional Debt Collectors Cooperative and Collection Agency Employment Group on Facebook brings global members together.

13. How to Market a Debt Collection Agency Business

Implementing promotional initiatives fuels a fledgling debt collection agency’s discoverability and client roster expansion. While organically establishing market viability takes patience, proactive outreach and advertising hasten traction.

Personal Networking

Leveraging one’s inner circle offers the most accessible channel for securing those inaugural accounts. Reach out to past employers, credit partners from previous industry roles, and professional organizations possessing receivables needs.

Offer friends referral incentives like gift cards to share your information when appropriate small business financing conversations arise. Customer testimonials also hold immense influence on prospective contracts weighing options.

Digital Marketing

On the digital front, multiple platforms enable affordable targeted messaging to ideally suited decision-makers. Google Ads easily locates lookup patterns of financing attorneys and bank executives within a defined radius. Facebook’s interest-targeting functionality aligns with credit issuers seeking subcontracted support.

- Google Ads – Geotarget debt collection keywords around a service area

- Facebook Ads – Target interest tags like “credit risk management”

- Launch a YouTube Channel – Share mini case study wins through video

- Guest blog for regional legal and finance blogs

- Start an agency LinkedIn Showcasing credentials

Traditional Marketing

Slow-burn grassroots outreach builds community awareness for debt collection players as well.

- Design eye-catching trifold mailers for households and businesses

- Sponsor community event booths to meet residents

- Place real estate and telephone pole advertisements

- Run:30-second radio mentions on local stations

- Advertise in weekly newspapers and church bulletins

Mixing digital and analog exposure toes the line between modern discoverability and old-school relationship building. Send custom collateral to past database contacts and cohorts while closely monitoring web traffic surges from each initiative. Attention attributed to marketing fuels the pipeline.

14. Focus on the Customer

Delivering exceptional service represents the clearest pathway toward securing ongoing client contracts and referrals in the debt recovery realm. Creditors have options when outsourcing delinquent accounts, establishing a compassionate, ethical approach differentiated from intimidating boiler rooms builds goodwill.

Display empathy and financial prudence during calls. Provide realistic payment plans showing principal balancing and terms while avoiding condescending tones. Follow up with email summaries and net seven-day payment reminders to debtors.

Channel compassion into action by proactively flagging and reassigning traumatic cases like grieving loved ones or job layoffs to internal crisis specialists. Clients remember these gestures when renewing or expanding retained placements.

The extra effort also feeds positive word of mouth between peer issuers. Satisfied capital partners open doors to new relationships upon enthusiastically endorsing your firm’s integrity and results.