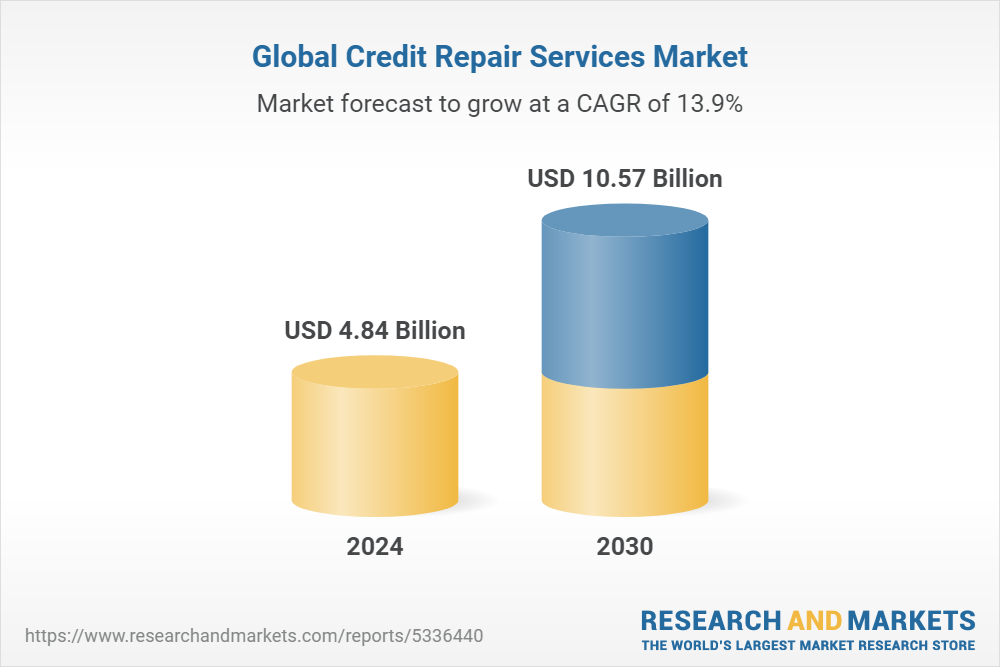

The credit score counseling industry has seen steady growth in recent years. According to IBISWorld data, the credit counseling and debt management services industry reached an evaluation of $6.6 billion in 2023. The industry is set to continue growing, making it a prime time to get involved.

Many consumers have limited financial literacy when understanding credit scoring models. By offering customized action plans, budget analysis, and debt management programs, credit counselors empower clients to take control of their finances.

This guide will walk you through how to start a credit score counseling business. Topics include market research, competitive analysis, marketing, registering an EIN, obtaining business insurance, and more.

1. Conduct Credit Score Counseling Market Research

Market research is essential to starting a credit counseling business. It offers insight into your target market, trends in the credit counseling business industry, and important changes to reading and managing credit reports.

Some details you’ll learn through market research as a credit counseling agency include:

- With mounting debt levels comes an interest in credit advice, especially for services like debt management, budgeting, and repayment plan development.

- A common service offered by an effective debt counselor service is a personalized financial plan.

- The average U.S. credit score currently hovers around 716 points.

- Scores below 700 suggest consumers likely require credit improvement assistance to qualify for favorable loans or low-interest rates.

- Up to 30 million Americans have what is considered “deep subprime” scores below 579, signifying serious existing credit challenges.

- Mortgage lending and refinancing activity levels are predicted to climb over the next five years.

- Significant portions of industry revenue stem from charging fees for customized financial action plans.

- Typical fees range between $25 to $100 charged every month.

- Technology utilization allows the highest-grossing credit counseling firms to serve larger volumes of customers online while minimizing overhead expenditures.

- Scalable software platforms can handle intakes for new clients, provide initial score assessments, and deliver personalized guidance or video lessons through client dashboard interfaces.

The combination of steady industry expansion and low barriers to client acquisition signals a favorable outlook for certified credit counselors. Entrepreneurs with robust financial counseling skills are positioned well to tap into this $1 billion sector.

2. Analyze the Competition

Thorough competitive analysis is key when assessing the landscape for a new credit score counseling venture. This should evaluate businesses that focus on building business credit and personal credit.

To analyze local competitors, start by identifying credit counseling agencies within a 20-mile radius. Check listings on Google Maps and Facebook Business directories, which rank options by reviews and engagement. Visit competitor websites to gauge their positioning, services mix, client specializations, and pricing models.

Sign up for consultations to experience their sales process first-hand. Take notes on strengths and weaknesses compared to your planned offerings. Ongoing monitoring of new player entries or service expansions is prudent as well.

Evaluating digital competitors is equally important for new e-counseling startups. Research national providers like Freedom Debt Relief and National Debt Relief that serve customers remotely. Review their client intake processes and account dashboards to inform your own planned tech stack.

Use SimilarWeb, BuzzSumo, and Semrush to analyze visitor traffic, lead conversion rates, and organic rankings across top online credit counseling sites. This quantifies website performance and can pinpoint SEM optimization opportunities.

Local and national competitors each offer unique indicators to shape your ideal value proposition. Blend personalized services, niche specialties, strong web conversion, and effective SEO to craft a differentiated brand.

3. Costs to Start a Credit Score Counseling Business

When starting a credit score counseling venture, entrepreneurs must budget for both initial launch costs and recurring expenses. Careful financial education and planning will prevent common cash flow issues faced by new agencies.

Startup Costs

Total expected start-up costs for a credit counselor are typically between $2,000-$5,000. The largest upfront costs include:

- Incorporation paperwork and licensing – $750 Complete LLC filing or corporation paperwork through online services ($149). Acquire necessary state licenses for credit counseling or financial advisory services in your jurisdiction (fees vary).

- Office equipment & software – $1,000-$3,000 For brick-and-mortar, furnished office space and waiting areas.

- Website design & development – $1,500+ Have a professional site built that establishes credibility and trust with financial services clients if coding expertise is limited.

- Insurance policies – $500-$2,000 Incorporate basic business insurance coverage like commercial general liability to cover counseling sessions and professional liability protection.

Ongoing Costs

Ongoing monthly costs for day-to-day credit counseling operations largely include:

- Lease/rent if based in a physical office – $1,500+ monthly For newer e-counseling firms, coworking memberships offer more flexibility.

- Salaries for credit counselors or back office staff – $4,000+ monthly As caseloads grow, additional certified counselors must be brought on to serve expanding clientele.

- Advanced software subscriptions – $100-$500 monthly Upgrade tools to access enhanced client screening and credit analysis or onboard more users.

- Professional associations dues – $50-$500+ annually Consider memberships with trade groups like the National Foundation for Credit Counseling to access guidance and best practices.

- State license renewals – $100+

- Corporation fees – $500+ Maintain LLC status or incorporate as a formal business entity each year.

Identify any niche specializations or growth strategies that may necessitate further expenses. Careful financial planning is key when starting your own business.

4. Form a Legal Business Entity

When establishing a legal structure for a credit score counseling venture, entrepreneurs must weigh options like sole proprietorships, partnerships, corporations, or limited liability companies (LLCs). The right choice comes down to liability protections, tax implications, and ease of management.

Sole Proprietorship

A sole proprietorship provides the simplest route for solopreneurs, requiring only a DBA without formal company registration. However, this exposes personal assets to any potential counseling-related liabilities.

Partnership

Partnerships allow co-owners to combine expertise but still lack LIABILITY shields beyond insurance policies. Corporations have higher setup costs with extensive filing requirements but enable company shares and equity incentives.

Limited Liability Company (LLC)

For most credit counseling startups, forming an LLC offers the best of all worlds. LLC registration protects personal assets from any professional liability risks that could arise from working directly with finances. LLC income passes directly to the owners’ tax returns as well, avoiding corporate double taxation.

Corporation

A corporation is the most advanced and protected business structure for a debt counseling business. While it offers protection of personal assets during financial or legal issues, it’s also the most costly and complicated business model to form.

5. Register Your Business For Taxes

Before accepting any clients, new credit score counseling companies must register for federal and state taxes to legally operate. The first step is to acquire an Employer Identification Number (EIN) from the Internal Revenue Service (IRS).

An EIN acts like a social security number for your business. This unique nine-digit number identifies the company for all tax-related filings and reporting. Even if you start as a sole proprietor without official employees, obtaining an EIN is required to open business bank accounts or apply for licenses.

Luckily the EIN application process only takes a few minutes online, simply:

- Navigate to the IRS EIN Assistant

- Select the option to “View Additional Types, Including Tax-Exempt and Governmental Organizations”

- Choose “Financial Institutions” from the entity list and follow the short questionnaire.

- Submit

Once submitted, the EIN is immediately displayed and emailed to you. The online form is more efficient than mailing paper applications which can take weeks to process. There is no fee to obtain this essential number.

With your EIN in hand, visit your state’s business tax office to understand if you need to register for a sales tax permit or use a tax license. For financial services like credit counseling, sales tax may not apply but requirements vary across jurisdictions.

6. Setup Your Accounting

Proper financial record keeping is critical for credit score counseling agencies right from launch. Robust accounting ensures full legal compliance, efficient client billing, and scalability over time. The right systems also provide real-time visibility into the key financial health metrics of a fledgling small business.

Accounting Software

Begin by establishing dedicated business bank accounts and credit cards, separate from any personal finances. This simplifies tracking all counseling-related income and expenses. QuickBooks accounting software then enables automation by directly importing transactions from financial accounts.

Hire an Accountant

As revenue grows, working with an experienced accountant or bookkeeper provides an extra layer of oversight while freeing up your schedule. Typical monthly tasks handled include reconciling bank/credit accounts, producing financial statements, managing payables/receivables, and identifying growth opportunities.

Open a Business Bank Account and Credit Card

Open a business bank account to remain accountable for business expenses. Separating personal and business spending ensures ease of organization during tax season. Applying for a business credit card even as a new entrepreneur simplifies tracking expenditures. This also helps you establish credit as a business through credit bureaus.

7. Obtain Licenses and Permits

New credit counseling companies must ensure they acquire all required state and federal permissions to legally provide services. Find federal license information through the U.S. Small Business Administration. The SBA also offers a local search tool for state and city requirements.

Most states mandate a specialty credit counseling or credit services license to offer debt management advice. For example, the Texas Application for Credit Access Business License costs a $250 application fee plus $100 annual renewals. Licensing ensures counselors meet expertise requirements around financial regulations.

Cities or counties may require general business licenses for all commercial operations including financial services. Denver’s business licensing portal offers low-cost renewals for credit agencies. Display prominent signage as dictated by local authorities.

501(c)(3) nonprofit status makes credit counseling groups eligible for tax-deductible donations. Given extensive IRS applications and compliance rules, most agencies operate as for-profit businesses initially before pursuing nonprofit designations.

The Federal Communications Commission (FCC) mandates registration for any debt relief services advertising on phone/TV to protect consumers from scams. While credit counseling differs from debt settlement, registering an FCC business name enables all promotional opportunities legally.

The Counseling Center Licensing Dashboard by the US Department of Justice provides state-by-state resources on credit advisor credentialing. Adhering to state statutes around permissible fees, contract structures, and licensed activities reduces compliance risks.

8. Get Business Insurance

Securing adequate business insurance coverage is a crucial protective step for new credit score counseling agencies. Various policies can shield owners against major liabilities that might otherwise bankrupt unprotected firms or drain personal assets.

A range of common scenarios pose potential financial risks lacking proper insurance:

- Client lawsuits stemming from allegations of counseling negligence, data breaches, or violations of service terms buried in fine print could lead to monumental damage awards.

- Building disasters like floods, fires, or burglaries that destroy sensitive client data or physical offices often involve massive repair and recovery costs without support from insurance claims.

- On-premises worker injuries may trigger expensive medical bills and improper termination litigation if policies are not in place.

Purchasing a basic general liability insurance policy presents the minimum recommended level of protection, with typical monthly premiums of around $50 from providers like Next Insurance. Various additional coverages merit consideration as well, including professional liability specific to advisory services.

The application process first involves careful research into state minimum requirements and the array of policy options available through insurance marketplaces like CoverWallet. The necessary level of coverage hinges on factors like total client volumes, the sensitivity of data assets retained, office sizes, and employee headcounts.

Making wise investments in robust policies early on provides credit counseling entrepreneurs welcome peace of mind to focus on daily advisory work rather than risk scenarios. This prevents personally funding crisis responses or legal settlements down the road.

9. Create an Office Space

Securing dedicated office space provides a professional backdrop for consultations while allowing credit counseling staff room to handle administrative tasks beyond home environments. The right facilities strengthen brand perception while accommodating business needs.

Home Offices

Solopreneurs can minimize costs by initially leveraging home offices or spare bedrooms for meetings with local clients. While convenient for bootstrapping agencies, conducting sensitive financial consultations in personal residences may detract from credibility for some.

Coworking Spaces

For fledgling agencies focused on virtual counseling options, coworking memberships through providers like WeWork grant valuable flexibility. Customizable tiers from $300 per desk monthly provide turnkey office infrastructure from mailing addresses to conference rooms available as needed to host local sessions.

Commercial Offices

Long-term growth plans may warrant eventual commercial office leases to accommodate support teams in a scalable corporate environment (over $10,000 monthly). This also projects an enterprise-level brand image for global service expansion.

10. Source Your Equipment

Launching a credit counseling company requires minimal physical equipment thanks to lean virtual business models. Instead, software tools and services substitute traditional assets. Savvy sourcing saves thousands over conventional furnishings.

Buying New

Focus new equipment budgets on robust client devices like laptops ($500+), tablets ($200+), or dual monitors rather than extensive office furniture. Reliable high-speed internet ($50+ monthly) enables seamless video consulting. Debt management software (from $20/month) centralizes client records.

Buying Used

Gently-used electronics via eBay cut costs substantially. Search local inventory on Craigslist and Facebook Marketplace for discounted supplies like file cabinets, backed chairs, or small conference tables for home offices. Charities like Habitat for Humanity also resell furniture.

Borrow, Lease, or Rent

Minimize large capital expenses through sharing services. Local libraries and community centers offer occasional free meeting room rentals.

11. Establish Your Brand Assets

Crafting a strong brand identity is crucial for credit score counseling firms to stand out amidst national debt relief providers and local competitors. Strategically moving beyond a generic business name to become a specialized authority within the financial advisory niche takes careful positioning.

Getting a Business Phone Number

Toll-free phone numbers project an established corporate image from launch. Services like RingCentral offer vanity business line options from $30 monthly. Call analytics help inform marketing. Route calls to cell phones or across distributed teams.

Creating a Logo and Brand Assets

A custom logo encapsulates the visual identity of a brand. Modern, approachable emblem styles for counseling agencies build trust. Looka’s AI logo maker generates tailored concepts matching specified moods like “reassuring” or “hopeful” for $20.

Printing Business Cards and Signage

Vistaprint provides affordable, high-quality business cards showcasing logos, taglines, and contact info to make memorable first impressions at networking events or client meetings. Retail signage offers comparable visibility.

Purchasing a Domain Name

The right domain imparts credibility and conveys focus areas to visitors. Aim for exact match names like CreditCounselingAgency.com from registrars like Namecheap. If taken, adjust with location or specialty descriptors.

Building a Website

Hiring web developers on freelance sites like Fiverr can provide affordable website build and customization options for those lacking coding expertise. But user-friendly drag-and-drop site makers like Wix also enable DIY website designs with stylish templates and built-in SEO guidance.

12. Join Associations and Groups

Joining key professional groups and associations accelerates networking and exposure for new credit score counseling ventures. Tapping into established community guides while raising local visibility.

Local Associations

State credit counseling alliances like the Credit Counselling Society organize annual conferences, lobbying efforts, and certification programs. Membership fees fund valuable initiatives. Regional chapters of the National Association of Certified Credit Counselors (NAC) also connect accredited specialists.

Local Meetups

In-person networking events create organic relationship-building opportunities with related professionals. Financial advisor meetups or small business mixers through Meetup provide warm introductions to potential partners. Look for regional fintech conferences or credit decision-maker trade shows to present services.

Facebook Groups

Industry-focused Facebook Groups foster ongoing idea exchange and advice access from peers nationwide. The Road to 800s Credit Score and 750+ Credit Journey And Debt Ditch Community offer networks of thousands. Participate consistently to become a trusted community voice.

13. How to Market a Credit Score Counseling Business

Implementing multifaceted marketing is pivotal for credit score counseling firms to continually expand local visibility and clientele. Balancing digital promotion with community networking and referrals ensures durable growth.

Referral Marketing

Early customers often intertwine personal and professional contacts who may then organically refer others in similar financial straits after achieving counseling success. Offering discounts on future services in exchange for client testimonials or endorsements further incentivizes supporters to share positive experiences.

Digital Marketing

- Google Ads campaigns can target consumers seeking related services like “credit repair near me”. Helpful for capturing web traffic from urgent searchers.

- Facebook Ad campaigns help segment audiences by factors like income, credit score range, home ownership goals or other struggling financial indicators using custom audiences then deliver video views, lead form sign-ups, and highly-tailored messages.

- Publishing ongoing educational content and financial tips blogs boosts organic visibility and expertise rankings online. Link to advice posts from social channels to increase site visits.

- YouTube video series could share concise guidance on improving credit scores, navigating debt settlements, or budget planning basics for millennials and generations lacking financial literacy foundations.

Traditional Marketing

- Print brochures and letters at libraries/colleges to outline services for locals. Schedule in-branch consult events or seminars during evening hours or weekends to be accessible.

- Radio spots on local stations reach commuters. Feature specialty offerings around mortgage preapprovals or military program assistance to resonate with niche demographics.

- Direct mail campaigns in Q1 target homeowners about to file taxes who may need assistance planning for major upcoming purchases or lifestyle changes in the New Year.

- Strategically placed transit ads along highway billboards commute paths or bus stops raise exposure to the masses.

Apply niche targeting layers across both digital and traditional channels to cut through noise. Let client referrals and community connections amplify reach further.

14. Focus on the Customer

Delivering exemplary customer service must remain the top priority for credit score counseling professionals every single day. Building trust and authentic rapport leads to higher client retention over time plus increased referrals as satisfied customers tell friends struggling with debt about your services.

Following up consistently also matters. Checking on progress hitting milestones in debt payoff calendars, reminding about upcoming creditor payments, or celebrating score increases keeps customers encouraged. Sending handwritten cards creates delightful surprises.

Consider incentivizing referrals from past clients by providing a discount on future services to keep the relationship strong. The most successful credit counseling firms earn 80%+ of new business from word-of-mouth praise. They focus relentlessly on customer happiness before profits.

In an industry hinged on sensitive money matters, forging personal connections that build financial confidence over months and years leads to exponential growth potential. New counselors should remain patient answering all questions while making each client feel like their only priority.