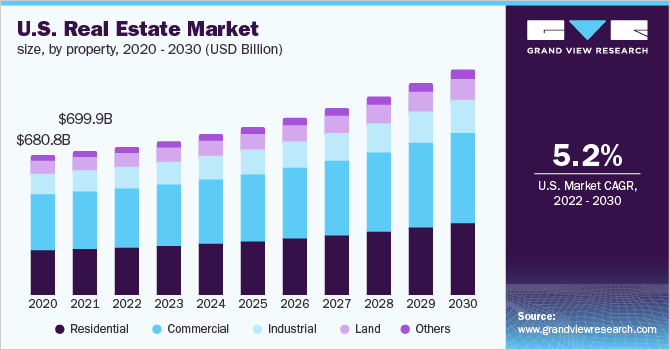

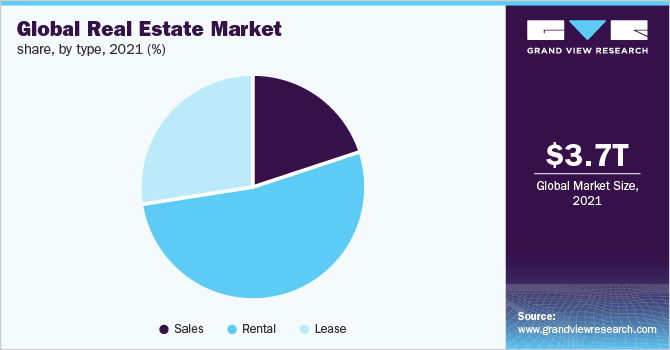

The global real estate industry is on the way up landing at a $3.69 trillion evaluation in 2021. With a compound annual growth rate (CAGR) of 5.2% projected from 2022 to 2030, now is a great time to get involved.

Rather than relying on sheer luck, strategic preparation can help aspiring real estate professionals build a steady client base. This includes developing a clear business plan, establishing healthy financial habits, and leveraging digital tools to boost visibility.

This guide will walk you through how to start real estate business. Topics include market research, competitive analysis, marketing, registering an EIN, forming a business entity, and more. Here’s everything to know about starting your own real estate company.

1. Conduct Real Estate Market Research

Market research is essential to forming a business plan for your own real estate business. It offers insight into your target market, market saturation, and trends among real estate investors.

Some details you’ll learn during primary and secondary market research in real estate include:

- While rising interest rates have cooled demand slightly, demographics continue to support real estate growth long-term.

- Millennials make up the largest share of home buyers at 43%, a proportion expected to expand further.

- The aging population will drive seniors’ housing needs as baby boomers enter their 80s.

- Immigration and household formation also contribute to residential rental or real estate for sale demand.

- On the commercial side, trends like remote work introduced uncertainty but also the potential to revamp office and retail spaces.

- Logistics real estate thrived with the surge in e-commerce, a trend poised to continue.

- With the right location and tenant mix, multifamily and industrial investments can provide stable cash flow.

- Affordable housing options such as RV parks and budget homes are growing in popularity.

- Aspiring real estate professionals have ample room for specialization.

- Referrals and repeat business are critical for success, favoring those skilled in marketing and building rapport.

- Commercial brokerage presents higher barriers to entry but also higher profit potential from leasing and sales commissions.

- Alternatives like real estate development or fractional ownership further segment the industry.

While real estate offers entrepreneurial freedom, commission-based income brings earnings volatility. Moreover, technology has raised consumers’ expectations around digital experiences even for high-touch services.

2. Analyze the Competition

Understanding the competitive landscape is critical for new real estate businesses. With over 1.5 million active agents in the U.S., competition is fierce for listings and buyers. Performing comprehensive competitive analysis should examine both local brick-and-mortar rivals as well as digital presence.

To analyze nearby real estate agencies:

- Gather their total agent count, average years of experience, transaction sides, specialty areas, brokerage models, and commission rates.

- Drive the neighborhoods they serve to observe for-sale signs and note listed properties on MLS.

- Subscribe to competitor newsletters and follow their social media for event announcements. This shows how they attract potential clients.

- Evaluating online competition involves assessing websites, search rank, reviews, and social media followings.

- Google key local terms like “Springfield real estate agent” and see where competitors appear versus your site.

- Check Facebook and Instagram follower counts along with engagement rates.

- Does their social content better educate and connect with followers?

- Beyond monitoring competitor activities, crunching market share data paints a clearer picture. Purchase trusted referral statistics by zip code from Market Leader.

- The “Ninja Report” compares your recent sales volume to other brokerages operating in your city or neighborhood.

- Look at which businesses they collaborate with to understand how you can maximize the efficiency of your real estate company. These can include title companies, home staging, property preservation, and more.

Ongoing competitive analysis should inform your marketing and operations strategy. Beat the competition by leveraging technology to create better digital experiences around searching, touring, or transacting real estate.

3. Costs to Start a Real Estate Business

When launching a real estate venture, both initial investments and recurring expenses must be planned to build a sustainable company. From licensing and equipment to marketing and insurance, tallying these costs in advance helps set realistic financial expectations.

Start-up Costs

- Expected start-up costs typically range from $2,000 for a bare-bones brokerage up to $100,000 or more for a brick-and-mortar franchise location.

- The foundation for any real estate professional is completing state prerequisites and passing the licensure exam, which runs from $100-$500 depending on location.

- Registering a business entity like an LLC costs $50-$500 plus state fees.

- Basic tech needs like a smartphone, laptop, and printer can be purchased for around $1,000 upfront.

- Many brokerages supply some of these tools so personal tech costs may be lower.

- Commercial real estate spaces average $20/sq ft in lease terms, with most small offices spanning 1,200-1,500 sq ft.

- Purchasing appropriate signage, furniture, desktop supplies, and networking during a first-year adds upwards of $15,000 in expenses.

- Brokers aiming for branded growth through franchise models like ReMax can pay between $50,000-$100,000.

On the lower end, solo agents working remotely under another broker often have under $5,000 in total first-year expenses. The difference depends heavily on individual business models and growth ambitions.

Ongoing Costs

- All real estate professionals need to budget for MLS access fees, professional associations like NAR, continuing education, local RE taxes or license renewals, and myriad transactions at $5,000-$20,000.

- Most brokers must split commission earnings with their sponsoring brokerage, often handing over 30-50% of earned commissions in exchange for licensing, training, mentoring, and lead generation support.

- Other frequent operating costs include database and CRM platforms, brokerage insurance plans, advertising, professional services like accountants or lawyers, office administration fees, and compensation for any hired staff.

4. Form a Legal Business Entity

When starting any venture, the legal structure carries important ramifications. Real estate professionals must weigh factors like taxes, personal liability, regulatory requirements, and growth ambitions when choosing between sole proprietorship, partnership, S-Corp, C-Corp, and limited liability company (LLC).

Sole Proprietorship

A sole proprietorship is a company owned by a single person, or by a married couple. Sole proprietors report income and losses on personal tax returns, avoiding the need to formally create a business structure. This saves paperwork but leaves all personal assets vulnerable to lawsuits.

Partnership

Partnerships allow the sharing of profits and managerial duties between two or more real estate professionals, governed by partnership agreements. Partnerships are best suited to family businesses. One downfall of a partnership is the lack of protection for personal wealth in the event of legal or liability issues.

Corporation

S-corps pass income directly to shareholders’ returns like partnerships, while also limiting liability exposure. However stringent ownership rules hindering outside investment make them poor fits for growing real estate ventures. C-corps have no ownership restrictions but face double taxation on profits and dividends. Moreover, real estate professionals receive no liability shield under corporations.

Limited Liability Company (LLC)

For these reasons, most realty ventures launch as LLCs which provide personal asset protection while allowing ownership flexibility. Profits and losses flow through to members’ tax returns per partnership rules, avoiding corporate double taxation. Legal and regulatory compliance burdens also pale compared to corporations.

5. Register Your Business For Taxes

Any venture conducting business transactions requires an Employer Identification Number (EIN), commonly called a federal tax ID number. Sole proprietors can use Social Security numbers for federal taxes, but EINs add legitimacy and simplify banking and licensing applications for real estate firms.

Registering for an EIN is free and can be completed online via the Internal Revenue Service in minutes. To begin, navigate to the EIN Assistant and select View Additional Resources for the application form. Choose Apply Online Now and confirm you are authorized to sign up for the business. Select view Additional Types, then Real Estate to correctly categorize the nature of your company.

You will need to provide basic information like business name, address, financial institution details owners’ legal names, and Social Security numbers. The online tool guides applicants through each required field. Be sure to specify your LLC or other business structure if already formally registered.

With an EIN secured, visit your state revenue or taxation site to register for sales tax collection rights and obligations. This allows you to charge and remit appropriate sales tax on services provided to clients.

For real estate professionals, mainly brokering the purchase and sale of property, sales tax often does not apply. But do confirm based on your state. Some jurisdictions do impose sales tax on broker commission fees over a certain threshold.

Take the time upfront to formally legitimize your real estate venture. An EIN and sales tax registration help present the professional image clients seek when trusting you with major financial transactions.

6. Setup Your Accounting

Careful bookkeeping provides the foundation for real estate professionals’ finances and taxes. While tempting to minimize paperwork and process home sales on the fly, disciplined tracking of every transaction safeguards your business. Revenue spikes and dips common in commission-based sectors make balancing the books vital.

Accounting Software

An automated accounting solution like QuickBooks simplifies the process using integration with bank/credit card accounts to log all sales and expenses. QuickBooks lets you generate financial statements, track revenue sources, reconcile balances, print checks, manage cash flow, and run essential tax reports with just a few clicks.

Hire an Accountant

Enlisting a knowledgeable accountant remains advisable as your go-to advisory for optimizing finances while staying compliant. A qualified accountant provides objective guidance on everything from business entity selection to mileage deductions to quarterly estimated taxes to retirement planning. Expect fees from $100-$300 per month for basic bookkeeping assistance scaling up to $2,000.

Open a Business Bank Account

Vital to smooth accounting is separating professional and personal transactions through dedicated business accounts. Keeping all real estate revenue, expenses, assets, and debts distinct simplifies tracking and protects your home/auto assets should the company face financial disputes.

Apply for a Business Credit Card

Apply for dedicated business checking/savings accounts along with company credit cards when formally creating your LLC or corporation. Business cards often offer higher limits thanks to income and assets tied directly to the venture versus personal credit scores alone.

7. Obtain Licenses and Permits

When gearing up to open a real estate company, properly registering with state and national regulatory bodies protects against fines or discontinued operations. Find federal license information through the U.S. Small Business Administration. The SBA also offers a local search tool for state and city requirements.

Foremost is securing a real estate license for all agents and brokers affiliated with the venture. Each U.S. state sets its prerequisites around age, education, and examination. Most mandate applicants first complete 60-90+ hours of approved pre-licensing education courses through local community colleges or online academies.

With educational background confirmed, candidates must then pass their state’s real estate salesperson or broker licensing exam. Broker licenses allow greater authority to oversee transactions independently versus salesperson licenses which must operate under a managing broker’s supervision.

Registered home inspectors assessing property conditions before sales commonly affiliate with brokerages. Depending on the state, home inspectors may require separate licensing or certification through application vetting and testing on structural and system fundamentals. Renewal, insurance, and bonding stipulations also apply in most areas.

Additionally, brokers frequently pursue separate licensure as mortgage loan originators (MLO) to qualify home buyers for financing. MLO approval includes federal registry, background checks, 20 hours of coursework, and passing national and state-level exams. So be prepared for plenty of work revolving around mortgages.

Finally, check local municipalities for any location-specific business permits around signage, occupancy, revenue collection obligations, and general commercial activity. Paying these permitting fees and staying current on all license renewals keeps the business operating legally as it ramps up transactions.

8. Get Business Insurance

Insuring your real estate venture shields against scenarios that could otherwise devastate unprotected firms. Policies cover expenses stemming from property damage, legal disputes, cyber incidents, and more that could potentially bankrupt uninsured brokerages. To make a real estate business profitable you must protect yourself and your employees.

For example, faulty wiring in your brokerage office sparks a blaze, destroying computers, listing files, and your entire space. Without insurance, replacing vital infrastructure and inventory to resume operations could cost well over $100,000.

Even if claims prove frivolous, five-figure attorney fees often result just to mount a defense. Alternatively, a data breach at your agency exposes clients’ financial account numbers. Legal fallout and cyber attack response costs could again outpace many small firms’ ability to pay out of pocket.

Business insurance fills these coverage gaps at fairly modest annual premiums, usually between $500-$5,000 depending on your policy’s size and scope. Common offerings like General Liability guard against bodily injury, property damage, and related legal expenses stemming from your business dealings up to set limits.

Professional Liability helps defray costs tied to mistakes, negligence, or errors in service during transactions. Commercial Property coverage handles workplace damage and inventory loss as mentioned. Cyber insurance is newer but wise given digital data’s crucial role in real estate.

9. Create an Office Space

Establishing a professional workspace lends legitimacy for real estate agents and brokerages while providing necessary meeting capacity. When scouting locations, weigh options like home offices, coworking spaces, retail suites, or traditional commercial buildings based on budget, team size, and client impressions.

Home Office

Solo agents can minimize overhead starting by designating a home office for conducting remote work. Deductible expenses like internet, certain utilities, and proportionate property taxes make residential offices cost-effective for under $100 monthly. In-person meetings with clients should be relocated to coffee shops or rented spaces to maintain privacy.

Coworking Office

Coworking spaces like WeWork allow small teams to share reception areas, meeting rooms, and amenities across various industries for maximum flexibility. Real estate is one of the most prolific sectors found in coworking locations since the on-demand model matches commission-based income swings.

Expect to pay roughly $300-$500 monthly for an assigned desk or private office in a coworking space plus scaling fees to reserve conference rooms or event spaces as needed.

Retail Office

For regular client meetings, retail spaces in shopping plazas mix public visibility and accessibility for realty boutiques at around $2,000-$4,000 monthly. Custom buildouts can establish an upscale brand identity. However, foot traffic rarely converts without additional digital marketing efforts.

Commercial Office

Over the long term, commercial offices offer the most control yet require substantial capital investment or loans to secure multi-year leases. Expect starting rates of $20 per square foot in suburban areas scaling past $60 for prime urban addresses. With creative buildouts, these spaces make fine showrooms for real estate deliveries.

10. Source Your Equipment

Launching a real estate venture requires few physical assets thanks to technology lowering barriers for remote work. Still, some equipment remains essential from smartphones to printers regardless of business model or location preferences.

Buy New

Buying brand-new equipment allows customizing devices to a firm’s exact needs while utilizing the latest features. Devices like iPhones, tablets, and laptops run $500-$2,000 when purchased upfront from Apple or electronics retailers like Best Buy depending on specifications.

Buy Used

Turning to used marketplaces like Craigslist, Facebook Marketplace and eBay expands affordability, particularly for printers, desks, and office furniture. Define must-have usage capacity or features then peruse local sellers’ listings nearby to avoid excessive shipping. Be ready to pay in cash and even rent a truck for large hauls.

Rent

Those wanting to mitigate upfront expenditures can rent basic tech monthly from stores like Rent-A-Center. However, total spending often exceeds just purchasing outright after a couple of years of payments. Leasing makes more financial sense for costly specialized equipment like high-volume printers or copiers costing thousands.

11. Establish Your Brand Assets

Cultivating a distinct brand identity helps real estate professionals stand apart in competitive markets flooded with agents offering similar services. Implement branding elements that consistently showcase your agency’s specialties and values across all touchpoints.

Get a Business Phone Number

Centralizing communications is key through a dedicated business phone line. Providers like RingCentral deliver call, text, and fax capabilities across mobile and desktop devices for $30 monthly. Route calls seamlessly from your cell to sound integrated.

Design a Logo

An eye-catching logo also brings instant awareness to listings and touchpoints. Looka’s logo maker helps brokerages design icons that encapsulate their vision through multiple concepts to choose from. Favored styles for realty ventures include abstract marks evoking ideas of communities or homes.

Print Business Cards

With a visual identity set, creating brand assets that align with the logo look brings consistency. Business cards, email signatures tied to your domain, and yard signs all influence first impressions. Vistaprint offers affordable, quality printing on these items featuring the company graphics.

Buy a Domain Name

Securing a domain name that matches your agency builds authority and recall. Short, simple handles like [YourName]RealEstate get snatched quickly. Once purchased, redirect the domain to initial single-page sites built through user-friendly platforms. Use vendors like Namecheap.

Design a Website

Outsourcing site development to specialized contractors found on Fiverr makes sense for those lacking tech skills. You can also design your site with Wix. With branding pillars in place, web developers translate vision into responsive, functional experiences that empower further marketing.

12. Join Associations and Groups

Plugging into local real estate networks builds invaluable connections for exchanging insights, prospects, and services. Industry associations, meetup events, and online communities all provide conduits for networking amongst fellow brokers and affiliated members.

Local Associations

Every U.S. region hosts Realtor associations coordinating area listings, training, lobbying, and more. Joining these nonprofits like the Austin Board of Realtors unlocks MLS access while integrating into regional brokerage circles. Most levy annual membership fees on individuals and brokerages ranging from $100-$500.

Local Meetups

Attending local real estate meetups facilitates direct relationship building through consistent face time. Sites like Meetup catalogue these recurring events from open houses to mastermind sessions allowing you to RSVP. Trade organizations like the Women’s Council of Realtors and the National Association of Hispanic Real Estate Professionals also convene frequent mixers.

Facebook Groups

Realty pros can further tap into digital communities inhabiting Facebook Groups. Some hyperlocal Buy/Sell/Trade groups provide members first looks at upcoming listings. Others like Real Estate Group and Real Estate Agent Referral Network & Marketing Tips foster idea exchange amongst seasoned agents nationwide.

13. How to Market a Real Estate Business

Implementing multifaceted marketing is non-negotiable for real estate professionals striving to continually expand their client roster and listings in an ultra-competitive sector. While leveraging existing connections and referral networks makes up the foundation, layering in advanced digital and selective traditional strategies pushes visibility further.

Personal Networking

Tap into your inner circle first when launching, as friends, family, and acquaintances already trust your character and skills. Offer reduced commissions or gift cards to happy buyers/sellers who refer new leads. This incentive gets the word spreading organically.

Digital Marketing

On the digital front, precision pays when trying to capture motivated site visitors and drive them to convert through tailored experiences. Useful approaches include:

- Google Ads – Target homeowners in surrounding zip codes most likely to sell soon through hyperlocal search and display ads.

- Facebook Ads – Retarget those browsing listings in a custom radius to your landing pages.

- Email Marketing – Import contacts to Mailchimp after events to share market updates.

- YouTube Channel – Post vlogs touring fresh listings or neighborhood insights.

- Blogging – Optimize site content around buyer/seller pain points and questions.

Digital Marketing

While digital mediums sidestep geographic limitations to find specialized audiences, traditional options better suit raising local visibility. Consider deploying:

- Direct Mailers – Send listing announcements or market projections to farms and suburbs.

- Door Hangers – Canvas target neighborhoods informing of specialized services.

- Chamber Membership – For networking with area professionals and sponsorship.

- Open Houses – Draw neighbors curious about renovations and realtor meet-and-greets.

A balanced blend of digital and traditional promotion sustains steady client inflow for converting both sellers and buyers at each stage. Assess efforts monthly and pour resources into highest highest-performing channels.

14. Focus on the Customer

Providing five-star service is what sets thriving real estate agents apart. In an industry dependent on local networking and referrals, impressing clients with responsive, thoughtful guidance throughout transactions spurs organic growth. Some ways to increase customer focus as you build a real estate business plan include:

- Home purchases mark the largest investment most families ever make.

- Expect nervous questions, last-minute paperwork, and endless showings to help buyers gain conviction before signing.

- Be patient answering concerns over inspections or financing issues.

- Celebrate successes closing on dream homes.

- Compassionate support sticks with families for years, earning repeat requests for selling and buying needs while recommendations to friends flood in.

- Simplify sellers’ transitions helping oversee appraisals, scheduling photographers/stagers, and tackling repairs needed to maximize list prices.

- Keep sellers apprised of showing feedback and offer realistic assurances if initial offers seem undervalued.

- Whether upsizing growing families or downsizing retirees, customers remember the agents who made the process smooth rather than stressful.

Consistently providing elite service cements trust in your capabilities and care for clients’ best interests. As an ambassador between complex transactions and major financial decisions, real estate agents who handle the human side of deals, as well as the business, prosper thanks to lifetime client relationships.